What happens to my HDB after I die? Understanding the CPF Home Protection Scheme

When we talk about insurance, the Home Protection Scheme is one that is easily overlooked.

Especially for couples and young families with new BTO flats, this is a scheme you should know of, as it serves as an added safety net, in case of unexpected events such as accidents or death.

Administered by the Central Provident Fund (CPF) Board, the Home Protection Scheme is compulsory for Singaporeans who pay their monthly home loan repayments via their CPF!

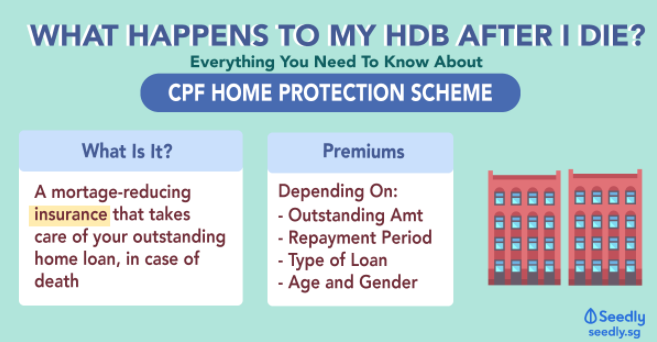

WHAT IS THE HOME PROTECTION SCHEME?

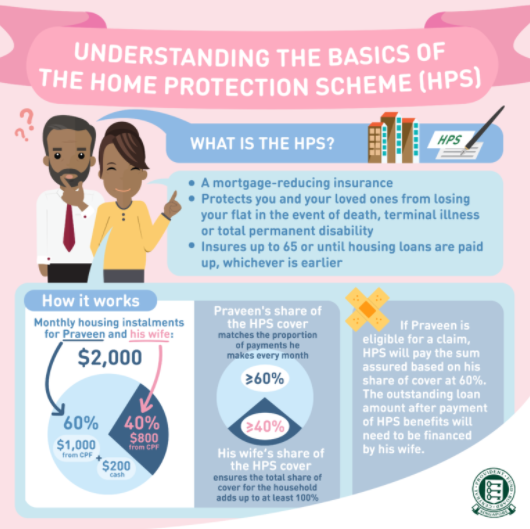

The Home Protection Scheme (HPS) is a mortgage-reducing term insurance that protects you and your family should you die or suffer a total permanent disability before the housing loan is fully paid. This means that in an event where something unexpected happens to you, your outstanding home loan will be paid for under the HPS.

DO I NEED TO BE INSURED UNDER HPS?

You have to be insured under HPS if you are using your CPF savings to pay for your monthly housing loan installments on your HDB flat. If you live in a private property, an executive condominium, or a HUDC flat, you don't need to be insured under the HPS.

If you are not using your CPF to service your home loan and still want to be covered under HPS, you can still apply for it.

WHAT DOES THE HOME PROTECTION SCHEME COVER?

[[nid:467345]]

The HPS provides coverage for the outstanding mortgage amount until the age of 65, or until your housing loans are fully paid up, whichever is earlier.

In the event of permanent incapacity or death, CPF will pay the sum assured, which will go towards paying your housing loan.

This way, your family will not risk losing the flat.

HOW MUCH DOES IT COST?

The premium of your Home Protection Scheme is determined by four factors. We will explain each factor in the following table:

| Factors | Reason |

|---|---|

| Outstanding home loan amount on flat | The higher your loan amount, the higher the premium you have to pay and vice versa. |

| Loan repayment period of flat | The longer the loan repayment period for the flat, the higher the premium. |

| Type Of Loan (concessionary rate or market rate) | HPS premium is more for those with HDB Market Rate loans compared to HDB Concessionary loans. |

| Age and Gender | The older you are, the higher your premium. Males tend to have to pay a higher premium. |

If you want to get an estimate on your HPS premium, you can use the Home Protection Scheme Premium Calculator.

A good point to note about the Home Protection Scheme is that you only need to pay for 90 per cent of your cover period. This means that if you plan to be covered for say, 20 years, you will need to pay premiums for the first 18 years.

WHO WILL PAY FOR THE HOME PROTECTION SCHEME PREMIUMS?

If you are under the Home Protection Scheme, the CPF Board requires 100 per cent of the outstanding home loan amount to be insured. Now here's the confusing part: Under HPS, CPF recommends that this coverage is spread according to your share of responsibility in repaying the mortgage.

[[nid:466479]]

What does this mean?

Your monthly housing installments are likely split between you and your partner. From the above example, Parveen is paying 60 per cent of the housing loan, while his wife pays 40 per cent. This means that the HPS cover for Parveen will have to be more or equal to 60 per cent, while his wife's share of HPS cover has to be more or equal to 40 per cent.

The annual premium will be automatically deducted from your CPF Ordinary Account to renew your cover. This is to ensure that you remain insured under the HPS.

EXCLUSIONS FOR THE HOME PROTECTION SCHEME

Similar to most insurance policies, you will not be able to make claims under HPS if the death or permanent disablement is due to self-harm or suicide. Additionally, if you are not in good health before the start of the HPS cover, you will not be able to make claims as well.

I DON'T WANT TO BE INCLUDED IN HPS, HOW CAN I BE EXEMPTED?

You can apply for HPS exemption if you already have one or more of the following insurance policies:

These policies must cover your outstanding housing loan up to the full term of the loan or 65 years old, whichever is earlier, in the event of death, terminal illness or total permanent disability. If your insurance policies used are discontinued or altered, CPF will extend a HPS cover to you based on the declared percentage you were exempted for. If you want to be exempted again, you need to reapply for it!

HOME PROTECTION SCHEME: IS IT ENOUGH?

A huge downside of having a HDB to call your own would be the liability of have a mortgage. On the bright side, mortage-reducing insurance like HPS ensures that this liability isn't passed down to your loved ones, in an event something unexpected happens.

What's more, the premiums are relatively affordable, and can be paid with your CPF ordinary account. Should you require more coverage on top of your HPS, you can also consider private insurances to protect your home!

This article was first published in Seedly.