The pros and cons of taking on debt to invest

PHOTO: Pexels

The idea of taking on debt to invest is not new to seasoned investors, and novice investors have been tempted by anecdotes of quick gains to jump on the bandwagon.

Known also as leveraging, it involves borrowing money — some examples being personal loans or other financial instruments — to invest and increase potential returns on your investment. This could be done when the potential for returns is high and cost of taking debt is low.

The main reason investors and traders take on debt to invest is to increase and accelerate their returns. With borrowed capital, it enables you to supplement your initial investment outlay to what you’d ideally want to invest. With a larger investment capital, your investment returns would also increase in tandem.

The best day to buy into the market this year was 23 March 2020, the lowest point in the market. In an ideal scenario, many investors would look to buy low and sell high. However, this is easier said than done.

[[nid:509410]]

Few can catch the market right at the bottom and have the confidence to sell when the market is bullish and reaching new highs. This is why time in the market outweighs timing the market.

Even though you might have missed the March 23 boat, there will still be dips in the market, presenting an opportunity for you to enter. In the Singapore market, at the current prices, there are still many stocks trading at a discount.

When market opportunities arise, we might not have sufficient liquidity to make the most of it, even if we know the time is now. Taking on debt to invest could allow you to take advantage of an opportunity in the market, which could be gone by the time you have sufficient capital.

Win big, lose big.

We have to stress, using debt to invest can be very dangerous and no one can predict the market. While your gains can be maximised, your losses could similarly be magnified should your investments underperform.

Famous investor Warren Buffet has also advocated against taking on debt to invest. While it is possible to reap greater returns, you could also end up losing far more than intended when the market heads south.

Different investors have different risk appetites, investment goals, financial situations and preferences. A strategy that suits someone else, might not suit you.

Some investors might be able to take on debt to invest because they have the experience, know-how and financial ability to counteract the risks.

However, there are also experienced investors who would caution against taking on debt to fast-track their investment returns.

If you are new to investing, lack emergency funds, or simply do not have the confidence to do so, this is a risk that should not be taken. The current macroeconomic environment and sentiments of recession also does not give us much confidence about job security; it’s probably not the best time to gamble on your financial standing.

When you borrow at a lower interest rate and earn a higher return, you can pocket the gains. However, when you take on debt to invest, you have to make sure that the returns on investment is significantly greater than the cost of the loan.

For example, if you are expecting returns to be 7 per cent and the money borrowed incurs 4 per cent interest, you will be earning a 3 per cent return.

ALSO READ: Investing in Exchange Traded Funds (ETFs): A newbie's guide to getting started

If your investment underperforms with returns of 5 per cent, you will be earning just 1 per cent, which is as good as leaving that money in a savings account that has little to no risk.

Markets can be volatile and you face the risk of not just not just earning low returns, but also losing money.

The risk you are exposed to also largely depends on the type of investment vehicle you choose and higher returns come with higher risk. Stock markets and derivatives are considered to be risky, while fixed income products have lower risk.

Using borrowed money to invest (as opposed to your own savings) can come with additional fees such as processing fees, transaction fees and early (or late) repayment fees.

These are additional costs to be factored in eats into your returns.

There are other ways to boost your investment returns. Here are two tips for investors:

The power of compounding has been emphasised by investment experts, financial advisors and investment companies alike. You should strive to start investing as early as possible.

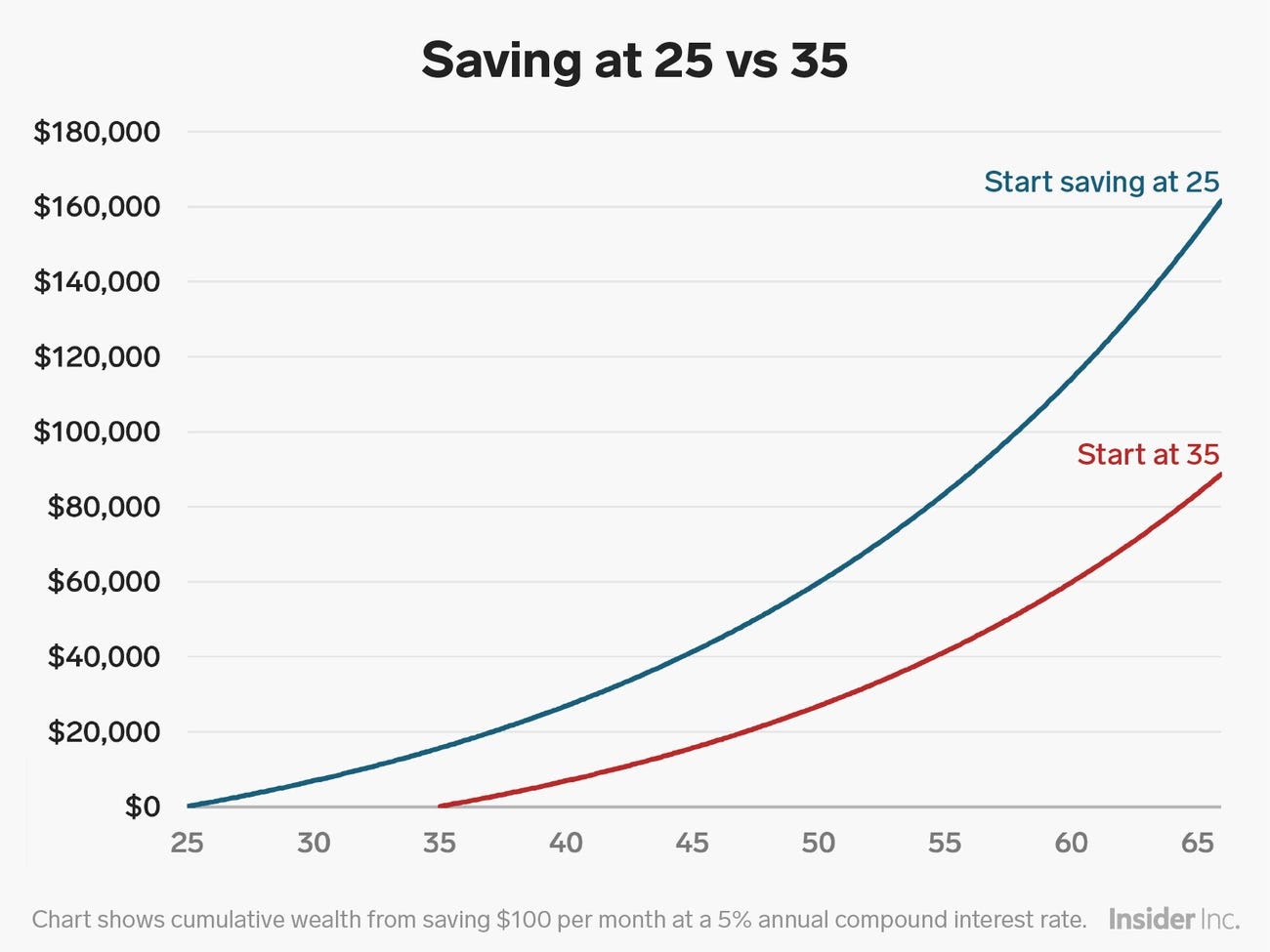

This allows you to ride out market volatility and to have more time in the market. You also reduce the opportunity cost of having your investment capital sitting in a low-interest bank account.

Based on investing $100 every month with a 5 per cent rate of return compounded annually, this chart shows the exponential growth your investments will enjoy when you have a 10 year headstart on your investment journey.

Borrowed money allows investors to invest more when they lack capital. If you want to increase your available capital to invest, you can strive to save more for starters.

The less you spend, the more you save. The positive impact of Covid-19 and working from home has helped to tighten some belts.

[[nid:510584]]

Other than spending less, you can also try to supplement income from your day job. You can take on a part-time job or start your own side-hustle.

Using debt to invest isn’t for everyone. You need to know what you’re doing as you can end up losing more than you intended to.

Do also keep in mind that while investing plays an important part in wealth accumulation, you should not forget the importance of other financial goals such as having an emergency fund and adequate protection from insurance, especially during challenging economic times like these.

This article was first published in SingSaver.com.sg.