How to cancel credit cards without hurting credit scores

PHOTO: Unsplash

Perhaps that enticing welcome gift promotion from a major bank doesn't excite you anymore, and your annual fee waiver negotiation rituals won't budge. Maybe those discretionary purchases spiked up because you feel that it's easy to swipe now and enjoy a refreshing bubble tea or travel to Paris.

But some credit card issuers can be annoying in that they pull the best benefits once you're in their ecosystem. If your credit card doesn't serve you well, it's time to get rid of it before you're charged with the annual fees.

Find out how to cancel your credit card painlessly in this guide.

Here are some telling signs that you need to say goodbye to your credit card:

Before you call the bank, make sure you follow the following steps.

Understand that your credit utilisation ratio-the amount of credit you're using compared to your total available credit-may increase if you cancel a card, which can negatively impact your credit score.

If you have other cards, ensure that the remaining available credit is sufficient to keep your utilisation ratio below 30 per cent, which is generally recommended for a healthy credit score. The goal is to aim for that sweet spot to show lenders you're not overly reliant on credit.

| Scenario | Total Credit Limit (S$) | Amount Owed (S$) | Remaining Credit Limit (S$) | Credit Utilisation Ratio (%) |

| Before Card Cancellation | 10,000 | 2,000 | 10,000 | 20 |

| After Card Cancellation | 10,000 (5,000 card canceled) | 2,000 | 5,000 | 40 |

This table clearly illustrates how cancelling a credit card with a S$5,000 limit affects your credit utilisation ratio, assuming you have a total debt of S$2,000.

When the available credit decreases from S$10,000 to S$5,000 while the amount owed remains constant, the credit utilisation ratio doubles from 20 per cent to 40 per cent.

That said, consider carefully whether you should cancel cards at this point. But if you're not that concerned about your credit score, you can proceed without regrets.

This UOB EVOL credit card used to be a great way for me to earn eight per cent cashback from Grab. However, a lifestyle change meant I no longer use Grab and this card.

Before you part ways with your card, do a rewards treasure hunt. Log in or glance over your statement to spot any unclaimed goodies-points, air miles, or cashback waiting to be redeemed. It's like finding money in a jacket pocket: use it or lose it.

Why so? Rewards are typically forfeited upon account closure. For example, if you have accumulated air miles, you might book a flight or upgrade a ticket. If you have vouchers or gift certificates to redeem, claim them before proceeding with the cancellation.

Go through your credit card statements to check any recurring charges, such as utility bills, subscription services, or insurance premiums, that are automatically charged to your card.

Before cancelling the card, switch these payments to another credit card or a different payment method, such as a debit card, e-wallet, or bank transfer.

This ensures you get all payments, which could lead to service interruptions, late fees, or negative marks on your credit report.

Clearing your balance means you can walk away, no strings (or fees) attached, and close that chapter with clarity. So ensure you fully pay off any outstanding balance on the card you intend to cancel.

This is crucial because you may be unable to close the account with a balance remaining, and leaving a balance could result in continued interest charges.

Once the balance is cleared, you can cancel without worrying about lingering financial obligations to the card issuer.

Alright, so you've decided to cancel your credit card and are calling the bank's hotline. Picture this: the customer service rep on the other end picks up, and naturally, they're curious about why you're cancelling your card.

This isn't them getting all nosy-it's just what they do, part of the routine. You can simply share that you aren't taking much action on the card these days. More often than not, they'll get the hint and back off.

Some banks might also have their customer service representatives try to persuade you to continue using the card, like offering a waived annual fee for life-just tell them you're not interested.

Here's a summary of the list of banks and how to cancel the card:

| Bank | How to Cancel |

| American Express | Call the customer service number on your card |

| Citibank | Call 6225 5225 |

| CIMB | Call 6333 6666 or submit form |

| DBS | DBS website chatbot |

| HSBC | HSBC website chatbot or app |

| Maybank | Call 1800 629 2265 |

| OCBC | Call 6363 3333 or submit form |

| POSB | Call 1800 339 6963 or write to them |

| Standard Chartered | SCB website or app |

| UOB | UOB TMRW app |

Cardholders can call the customer service number located on the back of their AMEX card. This is a direct and immediate way to request card cancellation.

| Credit Card Name | Contact Number in Singapore | Contact Number from Overseas |

| AMEX Platinum Card | 1800 392 1177 | +65 6392 1177 |

| American Express Platinum Credit Card | 1800 396 6000 | +65 6396 6000 |

| American Express Platinum Reserve Credit Card | 1800 392 1181 | +65 6392 1181 |

| American Express True Cashback Card | 1800 295 0500 | +65 6295 0500 |

| American Express Singapore Airlines KrisFlyer Credit Card | 1800 392 2000 | +65 6392 2000 |

| American Express Singapore Airlines KrisFlyer Ascend Credit Card | 1800 392 2000 | +65 6392 2000 |

| American Express Singapore Airlines PPS Club Credit Card | 1800 396 6888 | +65 6396 6888 |

| American Express Singapore Airlines Solitaire PPS Credit Card | 1800 396 6888 | +65 6396 6888 |

| American Express CapitaCard | 1800 723 1339 | +65 6880 1343 |

| American Express Rewards Card | 1800 296 0220 | +65 6296 0220 |

| American Express Gold Card | 1800 733 0833 | +65 6733 0833 |

| American Express Personal Card | 1800 732 2244 | +65 6732 2244 |

Cancelling a Citibank credit card is pretty straightforward.

Cancelling a CIMB credit card can be done in two ways: by phone or in person.

Option 1: Cancel by phone

Option 2: Cancel in person

Don't want to listen to hours of automated voice messages before getting connected to a customer service officer?

You can now cancel your DBS credit cards online.

Otherwise, you can cancel your card the conventional way by speaking to a customer service officer on the 24-hour DBS/POSB customer service hotline at 1800 111 1111 (from 8 am to 12 am). If you're overseas, call +65 6327 2265 instead.

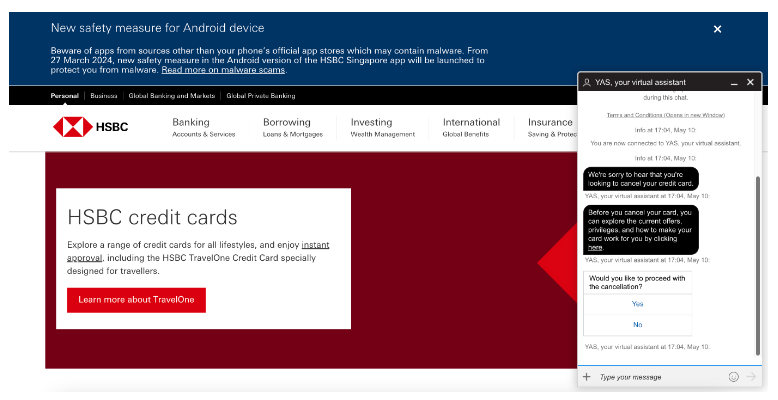

You can cancel your HSBC credit card in two ways: online via the HSBC banking website or by calling the HSBC Customer Service hotline.

Online cancellation

Cancellation via customer service hotline

To cancel a Maybank credit card in Singapore, you should follow these steps:

Banks want you to hold on to their credit cards. So, naturally, they will make it inconvenient for you to cancel them. To make matters worse, many banks like OCBC don't explicitly allow you to cancel your credit card online.

You'll have to call the customer service hotline, hold and wait in line for half an hour before speaking to a customer service officer.

To cancel your OCBC credit card, you'll have to call the OCBC customer service hotline at 6363 3333. If you are overseas, call +65 363 3333 instead.

Wait until all the announcements in English and Chinese are over, select your language (1 for English), enter your NRIC or card number, and then select 0 to speak with a customer service officer.

You can also terminate your credit card in person by doing the following:

To cancel a POSB credit card, you can do it via phone or send a written notice.

You can cancel your Standard Chartered credit card through the online banking website or mobile app.

After logging in, go to the menu bar and click on:

For those who have never bothered to use internet banking, you can simply call the Standard Chartered customer service hotline at 6747 7000 (8 am - 8 pm).

You can cancel your UOB credit card via the UOB TMRW mobile app.

First, log in to your UOB mobile app, then:

Otherwise, you can call the UOB customer service hotline at 1800 222 2121. If you're overseas, call +65 6222 2121 instead.

Go through all the automated menus and request to speak with a customer service officer by pressing 0, followed by 3 for credit card enquiries.

Yes, cancelling a credit card in Singapore can potentially hurt your credit score. This impact is due to changes in your credit utilisation ratio, which is a significant factor in determining your credit score. We covered this above.

Here are key points to remember:

And there you have it — you've officially Marie Kondoed your wallet. Pat yourself on the back for sparking joy (and a bit more space) in your pocket.

ALSO READ: 4 key questions to ask yourself before signing up for a credit card

This article was first published in MoneySmart.