Financial questions to ask your partner before you get serious

PHOTO: Pexels

In a survey on married people in Singapore, 90 per cent of couples said they had financial disagreements about half the time.

Whether you're considering moving in with your partner, getting married, or having a family together, you should ask your partner financial questions to avoid potential conflict down the line. If you both are not on the same page, making hefty financial decisions can be stressful.

However, having these discussions can help your relationship grow. To help you get started, we've listed the most important topics to cover.

One of the most important factors to consider is how much and what kind of debt your partner has. For instance, did your partner take out an education or business loan, or do they instead have a lot of credit card debt?

Discussing debt can be a sensitive topic for many, but you should have a general idea of how much your partner owes and how long it will take to repay the debt to avoid financial strain.

As a rule of thumb, "good" debt that can help you increase wealth over the long term (like education and home loans) is not a red flag until payments become unaffordable, but "bad" debt like credit card debt or personal loan debt can accumulate quickly and can potentially become a burden in the relationship.

If your partner owes quite a lot and it is hard for them to make monthly payments, your partner could look into obtaining a debt consolidation loan.

These plans consolidate all of your debt into one large loan, typically at an effective interest rate of 6.5 per cent - 10.5 per cent per year up to ten years, making them cheaper than many personal loans or a personal line of credit.

If your partner saves the recommended 20per cent of their monthly income, they could be on good standing for long-term financial health. However, if your partner doesn't save money, it might be worth knowing the reasons why. For instance, they could be investing their income in government bonds.

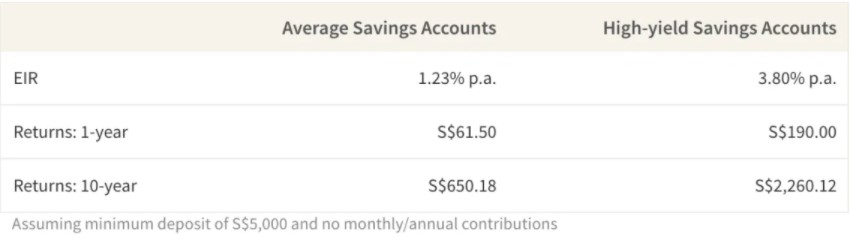

If your partner is looking to grow their savings, they could create a high-yield savings account to watch their savings grow. Alternatively, your partner could put monthly payments into a regular savings plan, which will invest in the stock market on their behalf.

Annual returns depending on your risk tolerance can be as high as 20.64 per cent — although please note that past results are not indicative of future results.

Another important question to ask your partner whether their mother and father split bills or one parent was responsible for paying all of the bills. Through this, you can understand more about what they might expect when it comes to splitting bills with you. This is especially pertinent if you plan to have a family.

Nowadays, it is quite popular to split the expenses based on your income so everyone pays a relative amount equal to their salary. That being said, make sure you discuss spending habits prior, as one person might spend more than the other.

Some married couples even have a joint bank account to pay for household expenses. The benefit of having a joint account is that you both will be able to access it and pay for bills.

Moreover, should something happen to you or your significant other, the funds are immediately available to either of you. However, joint accounts may not be the best for couples who have different ideas of how money should be spent and you value keeping your spending private.

ALSO READ: 3 finance questions to ask before a divorce

Knowing your partner's hobbies can help you see how they spend their money and what's important to them. For instance, if your partner loves outdoor activities, they might dedicate their recreational funds to equipment and vacations.

Alternatively, if they love online trading or the latest technology gadgets, they might spend their money on that.

This could be very important to know, as some hobbies are more expensive and even more dangerous, than others. For instance, if your partner likes to gamble recreationally, you may have to discuss how this could impact your relationship.

Knowing their plans can help you factor in your own finances. For instance, is your partner in the process of saving up for a flat? If so, does their budget and savings plan align with yours?

If you are both looking to buy a property in the next five years together, you both should be on the same page regarding a savings plan and what type of home you can afford.

On the other hand, your partner may want to start their own business or eventually move abroad. You should discuss these paths as they can change your financial plans.

If your partner has money habits that conflict with you and your spending or saving style, you may need to spend more time mapping out financial plans for long-term goals like buying a house or having enough money for your children.

Additionally, knowing what your partner spends his money on and where they see themselves a few years down the road can help you prepare for your future together. By asking these questions now, there will be fewer surprises when you go to make plans for the future.

This article was first published in ValueChampion.