Best travel insurance policies for places prone to natural disasters (2024)

PHOTO: Unsplash

When it comes to natural disasters, Singapore is a sheltered island. How sheltered? Based on data from 2023, we have the 4th lowest disaster risk in the world. So on this island refuge, it can be easy for us to feel detached from earthquakes, tsunamis and cyclones.

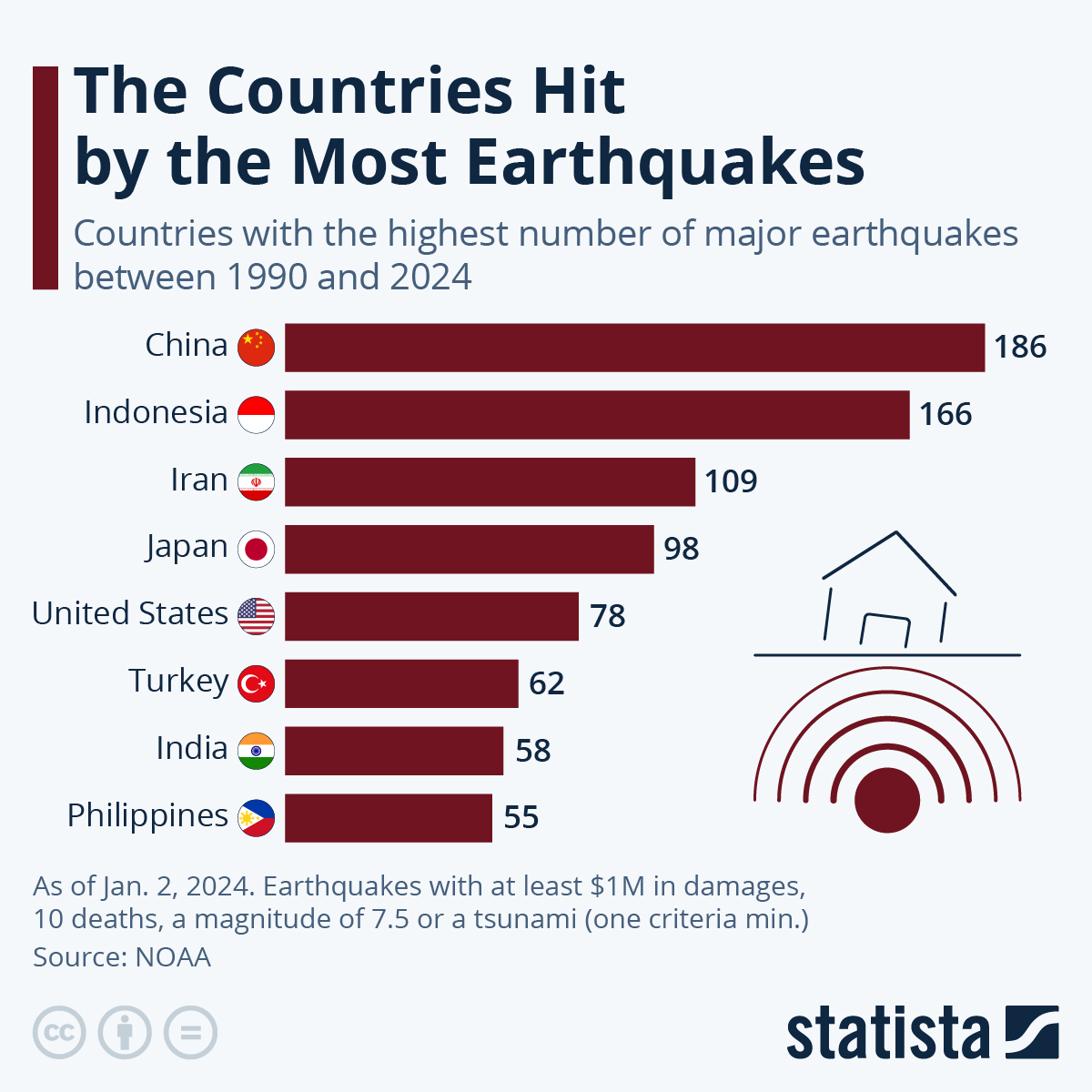

But it's a different reality for many of our Asian neighbours. For example, China lies where the Eurasian, Pacific, and Indian Ocean plates meet-a region with high tectonic activity.

Between 1990 to 2024, Statista reports that China recorded 186 earthquakes, the highest number in the world. According to the Global Facility for Disaster Reduction and Recovery, the earthquakes that hit China account for one third of destructive continental earthquakes globally. Yikes.

If you're travelling to earthquake-prone places like China, Japan or Bali, you want to make sure your travel insurance policy covers you in the event that your trip gets affected by natural disasters. Here's what you need to know.

You won't see a separate category for natural disaster coverage in travel insurance policies. Instead, insurers count natural disasters as one of several factors that may cause a trip cancellation, postponement, delay, or curtailment.

Let's assume you're going on a week-long trip to an Asean country. Here's a summary of the non-discounted costs and coverage of different travel insurance policies for trip disruptions and inconveniences due to national disasters.

| Travel Insurance | Maximum coverage due to events such as natural disasters | Premiums (ASEAN) |

| Citibank travel insurance (provided by DirectAsia—see policy wording) |

|

$32 – $60/week |

| FWD travel insurance |

|

$33 – $57/week |

| Tiq by Etiqa travel insurance |

|

$39 – $72/week |

| AMEX Travel Insurance (AMEX My Travel Insurance) |

|

$40 – $63/week |

| Singlife Travel Insurance |

|

$41 – $88/week |

| Bubblegum travel insurance |

|

$43/week |

| AIG travel insurance |

|

$48 – $125/week |

| Sompo Travel Insurance |

|

$64 – $83/week |

| MSIG travel insurance |

|

$67 – $125/week |

| Income travel insurance |

|

$68 – $109/week |

| DBS TravellerShield Plus Travel Insurance |

|

$75 – $122/week |

| Tokio Marine travel insurance (TM Xplora Plus) |

|

$78 – $101/week |

| AIA Travel Insurance (AIA Around The World Plus (II)) |

|

Enquire with an AIA Appointed Representative |

Before you buy your travel insurance, you need to do research on the following:

The first question to ask is what kinds of natural disasters the place you're visiting is prone to, if any. For example, is the area near an active volcano that might lead to a volcanic eruption? Does it sit on the Pacific Ring of Fire, where 90 per cent of the world's earthquakes take place?

At this point, also look out for disaster warning announcements — if you're forewarned that a natural disaster may occur but still go on the trip, you won't be able to make insurance claims.

Additionally, don't forget about natural disasters that you don't hear about as often, such as hail, ice storms, landslides, heat waves, and wildfires. These are important to consider because not everyone may consider them natural disasters — including your insurers.

Once you know what natural disasters your destination area is prone to, check if your travel insurance policy defines them as natural disasters. Some insurers may limit their claims to trip disruptions due to specific disasters such as typhoons, earthquakes and tsunamis. If you have to cancel your trip due to a heat wave but your insurance policy doesn't consider that a natural disaster, your claims won't be approved.

For example, here’s how "natural disaster" is defined by AIG travel insurance:

Comparatively, MSIG travel insurance listed fewer types of natural disasters as examples and described natural disasters as natural events with catastrophic effects:

A good rule of thumb is to choose a travel insurance policy with a broad definition of natural disaster. Don’t assume this is always the case, especially if you’re buying travel insurance from an airline.

Travel insurers generally define natural disasters as any event or force of nature which has catastrophic consequences on the environment, finances or human life.

Most types of natural disasters such as earthquakes, volcanic eruptions, floods, typhoons, tsunamis, hurricanes and so on can fall under this category if they are serious enough. If you feel light tremors causing no damage, you're unlikely to be able to make a claim.

Do note, however, that many insurers have exclusions on nuclear risks and exposure to nuclear radiation, even if this was caused by a natural disaster. For example, the Tohoku earthquake in 2011 caused the meltdown of three nuclear reactors, leading to the Fukushima nuclear disaster. Insurance would cover you for the earthquake, but may not cover you for the nuclear disaster.

The most important thing to note is that most insurers will not cover you if you already knew about the natural disaster risk in the area, but decided to book the trip or buy the travel insurance policy anyway. Insurers will usually include such announcements as travel advisories or warnings, such as this one from FWD:

So let’s say you have already read in the news that a volcano is about to erupt in a certain destination, and you go ahead and book a trip there anyway. If you end up having to cancel your trip because the volcano erupted, you are unlikely to get reimbursed for your travel expenses.

Recall that insurance policies don't have a claim category for natural disasters. Instead, you'll usually have to make a claim under one of the following:

Pro tip: You don't have to pore through each travel insurance policy wording to find out these claim limits! View them easily on our MoneySmart travel insurance comparison page.

What kinds of expenses can be claimed under the categories above? Typically, a travel insurance policy should pay for additional travel and accommodation expenses incurred should your trip be disrupted due to a natural disaster in the country you're in or travelling to.

If a natural disaster does occur while you’re travelling (choy!), contact your insurer as soon as possible, and preferably before incurring additional expenses like hotel bookings. They will advise you on the documentation you need to provide in order to make a claim, which might include receipts or police reports.

Finally, this has nothing to do with insurance, but it’s a good idea to call the Singapore Embassy in the country you’re in and ask for emergency contacts in case you need urgent consular assistance. You should also eRegister your overseas travel with the MFA so they can search for you if you go missing in any natural disaster (choy!).

As we mentioned earlier, your insurance claims won't be approved if you were forewarned about a natural disaster risk but chose to go on your trip anyway. So in this case, if you haven't booked your tickets yet, you probably shouldn't. But what if you've already booked your flight? Is it safe to go on your trip? Will you be refunded if flights are cancelled?

That was exactly what happened in October 2017, when it was announced that Mt. Agung in Bali was expected to erupt for over a month. After the last eruption in 1963 killed over 1,100 people, everyone in 2017 who booked a ticket to Bali was left wondering: Will I get killed if Mt. Agung erupts again? Should I still travel to Bali? If so, what can I do to protect my safety?

If a disaster warning surfaces after you've booked your tickets, here's what you need to know:,

ALSO READ: How to pick the best travel insurance plan

This article was first published in MoneySmart.