5 things to look out for when purchasing HDB resale flat

With the recent announcement by the Singapore government to allow greater flexibility of the Central Provident Fund (CPF) usage and housing loans for homebuyers, the HDB resale market has seen a sharp increase of 30 per cent in the number of units sold as compared to the first quarter of the year.

While many are jumping on the bandwagon, there is still a need to investigate the details before buying an older flat.

Here are five key factors that you may want to consider before going on the hunt for your next home.

HOW MUCH OF YOUR CPF CAN YOU UTILISE?

With the rising concern of adequate retirement funds among Singaporeans, new rules have been put into place in May to allow more flexible CPF usage for home purchases.

With this change, homebuyers can utilise their CPF to fund the entire Valuation Limit of their property as long as the remaining lease can cover the youngest buyer until the age of 95. If this criterion is not met, the amount of CPF allowed for funding the property will be prorated.

[[nid:458932]]

For example, if the homebuyer is 35 years old, the remaining lease of the resale flat must be at least 60 years before the buyer can fully utilise his or her CPF.

In the event that the remaining lease is less than 60 years old, the buyer may still proceed with the purchase, but the CPF that can be utilised will be prorated. To calculate the amount of CPF you can utilise for your housing needs, it is worth using CPF's free Housing Usage Calculator.

This new ruling not only implies that buyers must be concerned about the remaining lease of the flat but also how much additional cash or loan they have to set aside if they are unable to meet the requirement.

But does that really mean that it is worse off buying an older HDB flat even if you have to prorate your CPF usage? Considering that young couples are the hardest hit by new scenario, here is a comparison of how buying an old or newer flat can affect their financing.

As an illustrative example, the table below compares two 4-room HDB flats in Ang Mo Kio. One is an older flat and the other is a relatively new home.

For this example, we are using a couple with a younger spouse that is 28 years old. The couple's combined CPF available for property financing is $300,000.

From the above scenario, we can assume that the preference towards buying an older or newer flat very much depends on the availability of affordable financing for the buyers. Perhaps the concept of pro-rating CPF usage is not as unfavourable as the high price tag and small area size of newer units.

WHAT IS THE REMAINING LEASE OF THE FLAT?

Research has shown that property values tend to drop nearer the end of the lease. This is because financing restrictions are more likely during those times.

Not only will the maintenance of the aging flat be more costly but the potential for reselling may also be affected.

[[nid:462053]]

While some may pine for the Selective En bloc Redevelopment Scheme (SERS), a government en bloc programme which offers a compensation package for flats that are expiring, only 4 per cent of the Singaporean HDB flats have been earmarked for SERS programme.

If the flat you are about to purchase is not selected for SERS, it is more likely that it will be returned to the government when the lease expires, and this literally implies that the property will become worthless.

It is important to note that bank financing gets harder when the remaining lease of a flat reaches the 35 years mark.

Hence, if you are purchasing an older flat, you may need to consider how long you intend to stay and when you need to resell the unit before it becomes valueless.

Comparatively, newer flats are more marketable and the potential for reselling is also likely to be higher.

WHAT ABOUT THE HOME IMPROVEMENT PROGRAMME (HIP)?

The HIP is an enhancement programme that was introduced to improve older flats for public health, safety, and technical reasons.

If the flats you are shopping for is around 30 years old, the HIP overhaul will help to alleviate aging problems such as structural cracks and piping issues.

The programme can also include the upgrading of the toilet, main door, and gate and refuse chute hopper at a highly subsidised rate.

If a buyer purchases an older HDB flat which has yet to go through the HIP, the buyer can expect substantial savings on renovation down the road.

This is because the HIP programme is heavily subsidised by the Government (up to 95 per cent), flat owners are only required to pay between $630 to $1600 for the overhaul.

Those individuals that are not eligible for HIP and may require financing should consider shopping around for a renovation loans, as the most affordable options can save borrowers hundreds of dollars.

SHOULD YOU TAKE A HDB LOAN OR BANK LOAN?

There are pros and cons to every decision, and the choice between a HDB loan and bank loan depends solely on your personal preference, and of course, whether you qualify the long list of criteria laid down by HDB.

Here are some pointers that may help you decide.

A HDB loan is ideal for those who prefer stable repayment and would like to pay off the loan early.

On the other hand, bank loans tend to charge lower interest rates and can be easily refinanced every few years to guarantee the lowest rates possible.

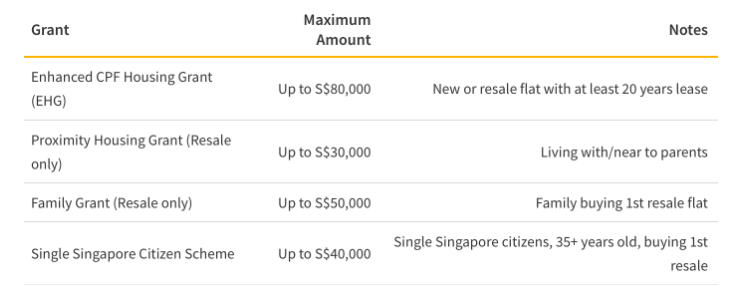

ARE YOU ELIGIBLE FOR GOVERNMENT GRANTS?

Starting in September, a change of housing grants was implemented and this also means that resale flat buyers may receive more financial support for their purchases.

These revised schemes benefit buyers and sellers, but come with strict terms and conditions.

To find out about your eligibility, visit HDB website or visit HDB office for enquiries.

DO YOUR HOMEWORK BEFORE GOING SHOPPING FOR AN HDB FLAT

Buying an older HDB flat in Singapore can be a great way to find an affordable home.

With that said, we strongly recommend that you conduct thorough research and due diligence in order to maximise the value of your investment.

While Government policies such as new CPF rules, housing grants and financing are opening up options for residents to purchase older HDBs with ease, buyers must also exercise caution when considering the long-term value of the property.

This article was first published in ValueChampion.